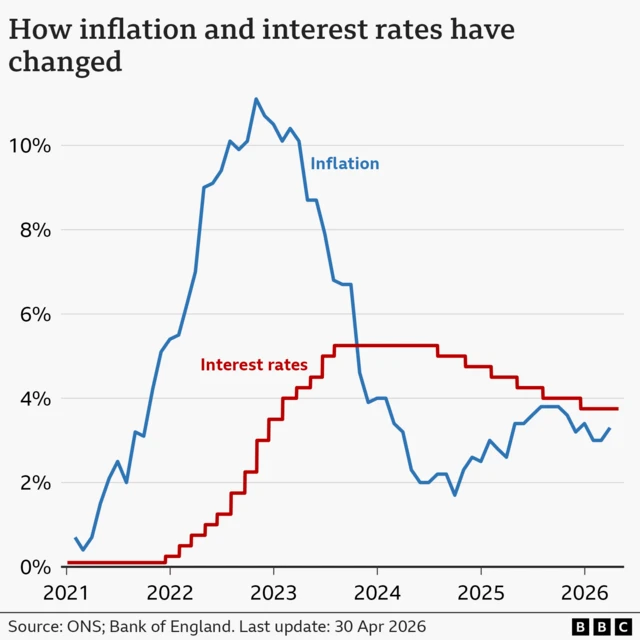

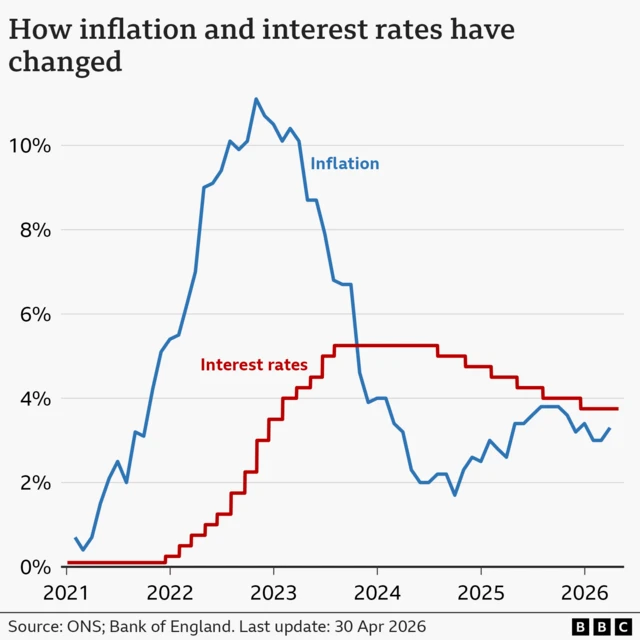

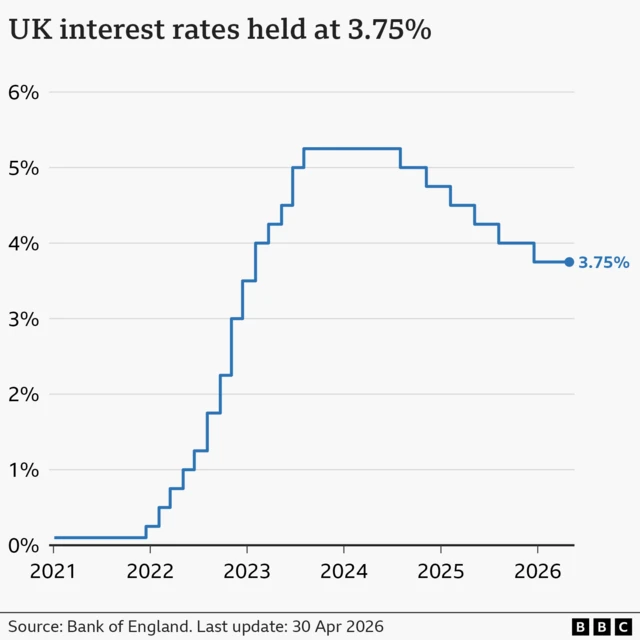

Bank of England holds UK interest rate at 3.75%, but hints at rises to comepublished at 14:22 BST 30 April

Image source, PA Media

Image source, PA MediaThe Bank of England has held the interest rate at 3.75%, but signalled rates could rise later this year owing to inflationary pressures from the Iran war.

Here's an overview:

- The Bank's nine-member rate-setting committee voted 8-1 in favour of holding the rate, with the Bank's chief economist Huw Pill voting for a rise to 4%

- However, in its announcement, the Bank says further rises were likely and pointed to the possibility of "forceful" rises to come

- Bank of England Governor Andrew Bailey stressed how difficult it is to predict which way things will go, due the volatility caused by the Iran war and its impact on energy prices - we've looked at three scenarios examined by the Bank

- Chancellor Rachel Reeves said the UK is in a "stronger position" in relation to the Iran war due to choices Labour has made

- But shadow chancellor Mel Stride said Reeves has "weakened" the UK economy and left it "vulnerable" to an energy shock

We’re ending our live coverage now, but you can read more in our full article here.